BÁO CÁO TÀI CHÍNH CÔNG TY honda motor

Bạn đang xem bản rút gọn của tài liệu. Xem và tải ngay bản đầy đủ của tài liệu tại đây (228.45 KB, 20 trang )

IV: FINANCIAL ANALYSIS OF HONDA MOTOR COMPANY:

4.1: Table of data.

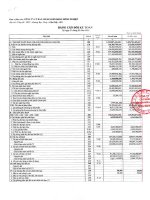

4.1.1. Balance Sheets.

Yen(millions)

Total current assets

Finance subsidiariesreceivables, net

Investments and

advances

Net property on

operating leases

Net property, plant and

equipment

Other assets

Total assets

Total current liabilities

Long-term debt,

excluding current

portion

Other liabilities

Total liabilities

Total Honda Motor Co.,

Ltd. shareholders'

equity

Noncontrolling interests

Total equity

Total liabilities and

equity

FY2010

4,613,724

FY2011

4,690,047

FY2012

4,739,086

FY2013

5,323,053

FY2014

5,771,266

2,361,335

2,348,913

2,364,393

2,788,135

3,317,553

642,681

639,932

623,607

668,790

817,927

1,308,147

1,357,632

1,472,757

1,843,132

2,236,721

2,086,663

1,939,356

1,973,458

2,399,530

2,818,432

616,565

11,629,115

594,994

11,570,874

3,419,130

3,568,192

3,579,759

4,089,004

4,711,329

2,313,035

2,043,240

2,235,001

2,710,845

3,234,066

1,440,520

7,172,685

1,376,530

6,987,962

1,454,937

7,269,697

1,630,085

8,429,934

1,563,238

9,508,633

4,328,640

4,449,975

4,392,226

5,043,500

5,918,979

127,790

132,937

125,676

161,923

194,419

4,456,430

4,582,912

4,517,902

5,205,423

6,113,398

11,629,115

11,570,874

614,298

612,717

660,132

11,787,599 13,635,357 15,622,031

11,787,599 13,635,357 15,622,031

Table 4.1: Balance Sheets

4.1.2. Income Statements.

Yen(millions)

FY2010

FY2011

FY2012

FY2013

FY2014

Net sales and other

operating revenue

8,579,174

8,936,867

7,948,095

9,877,947 11,842,451

Cost of sales

6,414,721

6,496,841

5,919,633

7,345,162

8,761,083

Selling, general and

administrative

Research and

development

Operating costs and

expenses

Operating income

Other income

(expenses)

Income before income

taxes and equity in

income of affiliates

Income tax expense

Equity in income of

affiliates

Net income

attributable to

noncontrolling

interests

1,337,324

1,382,660

1,277,280

1,427,705

1,696,957

463,354

487,591

519,818

560,270

634,130

8,215,399

8,367,092

7,716,731

363,775

569,775

231,364

544,810

750,281

-27,577

60,773

26,039

-55,919

-21,341

336,198

630,548

257,403

488,891

728,940

146,869

206,827

135,735

178,976

252,662

93,282

139,756

100,406

82,723

132,471

-14,211

-29,389

-10,592

-25,489

-34,642

Net income

attributable to Honda

Motor Co., Ltd.

268,400

534,088

211,482

367,149

574,107

Basic net income

attributable to Honda

Motor Co., Ltd per

common share

¥147.91

¥295.67

¥117.34

¥203.71

¥318.54

9,333,137 11,092,170

Table 4.2: Income Statements

4.2.

Analysis of the financial structure of the company.

4.2.1. Analysis of structural properties.

CONSOLIDATED BALANCE SHEET (assets)

Total current

assets

FY2014

FY2013

FY2012

5,771,266

5,323,053

4,739,086

Unit: Yen (millions)

Difference

±

%

2014/2013

448,213

8.42

Difference

±

%

2013/2012

583,967

12.32

Finance

subsidiariesreceivables,

net

3,317,553

2,788,135

2,364,393

529,418

18.99

423,742

17.92

Investments

and

advances

817,927

668,790

623,607

149,137

22.30

45,183

7.25

Net property

on operating

leases

2,236,721

1,843,132

1,472,757

393,589

21.35

370,375

25.15

Net property,

plant and

equipment

2,818,432

2,399,530

1,973,458

418,902

17.46

426,072

21.59

Other assets

660,132

612,717

614,298

47,415

7.74

-1,581

-0.26

Total assets

15,622,031

13,635,357

11,787,599

1,986,674

14.57

1,847,758

15.68

Table 4.3 Analyzes the structure of assets.

Looking at our target assets reflects the scale of the Honda company is relatively large, with a

manufacturing company is a large-scale analysis shows that the stature and growth commensurate with

a leading company the world in the field of industrial production. Through our tables show total assets

increased slightly in 2013 compared with 2012, an increase of ¥1,847,758 million, equivalent to

15.68%. By 2014 the total assets of ¥15,622,031 million, an increase of 14.57% compared to 2013.

This shows that the size of the company's capital increase, production and business scale has been

expanded.

Figure 1: Graph showing total assets (2010-2014).

In 2013, Finance subsidiaries-receivables, net increase of ¥423,742 million, an increase of

17.92%. This shows that companies with capital accumulation in the checkout process, so companies

need to take steps to reduce the amount receivable.

Investments and advances have increased slightly from ¥623,607 million in 2012 increased by

¥668,790 million in 2013, with a growth rate of 7.25%. This shows that the company has invested to

expand its market to seek long-term returns.

Net property plant and equipment with a strong ¥426,072 million, with a growth rate of

21.59%, showing that the technical facilities of the company have been strengthened, the production

scale of the company is increasingly expanding. In addition, the Total current assets task in 2013 was

¥5,323,053 million rose to ¥583,967 million rate is 12.32%, this factor accounts for the largest

proportion of the company.

By 2014, Total current assets task increased ¥5,771,266 million rose ¥448,213 million

equivalent of 8.42%. The increase had a decrease compared to 2012 was 12,32%. Finance subsidiariesreceivables, net increased by 18.99% or ¥529,418 million compared to 2013.

Investments and advances increased strongly to reach 817,927 million yen, an increase of 22.30%, this

increase is much higher compared to 2012 which suggests that companies tend to invest very high. Net

property, plant and equipment increased by ¥418,902 million increase of 17.46%. Compared to the

fifth floor at 2012 - 2013, the growth rate tends to decrease.

So from the above analysis we can conclude that the asset structure of the company is relatively

reasonable, but it can not be concluded that the financial situation of the company as well. As a

business with good financial situation does not only manifest in reasonable structural properties, but

also to have a capital to form fixed assets including structured legal and appropriate.

The capital structure analysis indicates the ability to financially sponsor of the company as well as the

degree of autonomy of the business or the difficulties that the company faces. Therefore, we must

continue to carry out structural analysis and capital volatility of the Company.

4.2.2. Analysis of scale and capital structure.

Based on data from the accounting balance sheet in 2012, 2013, 2014 tabulation analysis

of the changes in the size, capital structure is as follows:

FY2014

FY2013

FY2012

Values

Values

Values

Total current

liabilities

4,711,329

4,089,004

3,579,759

622,325

15.22

509,245

14.23

Long-term debt,

excluding

current portion

3,234,066

2,710,845

2,235,001

523,221

19.30

475,844

21.29

Other liabilities

1,563,238

1,630,085

1,454,937

-66,847

-4.10

175,148

12.04

Total liabilities

9,508,633

8,429,934

7,269,697

1,078,699

12.80

1,160,237

15.96

Total Honda

Motor Co., Ltd.

shareholders'

equity

5,918,979

5,043,500

4,392,226

875,479

17.36

651,274

14.83

194,419

161,923

125,676

32,496

20.07

36,247

28.84

6,113,398

5,205,423

4,517,902

907,975

17.44

687,521

15.22

15,622,031

13,635,357

11,787,599

1,986,674

14.57

1,847,758

15.68

Indicators

Noncontrolling

interests

Total equity

Total liabilities

and equity

Difference

±

(2014/2013)

Difference

%

±

(2013/2012)

%

Table 4.4: A breakdown of scale, capital structure.

Based on the data above table shows:

In 2013, the total capital of the company is ¥13,635,357 million, an increase of 15.68%.

In particular, the Total current assets 14.23% increase compared with 2012. Long-term debt,

excluding current portion increased by ¥475,844 million, 21.29% respectively. This causes

increased Total liabilities significant number 1,160,237 million yen, an increase of 15.96%

compared to 2012.

In 2012 Total Honda Motor Co., Ltd. shareholders' equity was ¥4,392,226 million, by

2013 this number increased to ¥5,043,500 million. So there is a heap of additional capital

contributions from shareholders to increase investment in business expansion.

Total resources of Honda Motor Company Ltd. in 2014 was ¥15,622,031 million, an

increase of ¥1,986,674 million to increase the proportion of 14.57%. In particular, increased

liabilities ¥1,078,699 million for the 7.91%. The proportion of liabilities is 61.82%, down

0.96% compared to 2014. Sources equity increased to ¥907,975 million rate is 6.66%: The

proportion of equity is 38.18%, up 0.96% compared to 2013 This shows the funding policy of

the company is using its capital, this is the company policy is maintained through Honda Motor

Ltd many years, and increasingly deliver better results, it is evident in the financial position of

the company improved throughout 2014.

- Liabilities:

Total current liabilities increased to ¥622,325 million, rate is 4.56%, increasing the

proportion of 0.17%, respectively, from 29.99% to 30.16%, still accounts for the largest

proportion of liabilities.

Long-term debt, excluding current portion tends to increase with ¥523,221 million, rate

is 3.84%, the proportion of long-term debt liabilities in 2014 is 20.70%, up 0.82% compared

with the 2013. Meanwhile, Other liabilities ¥66.847 million decrease to 0.49%, rate reduction

in 2014 has been very well managed company.

- Equity:

Figure 2: Graph showing equity (2010-2014).

Increased in all parts, in the capital owners, ¥907,975 million increase with growth rate

is 6.66%, 39.13% proportion of equity ownership. Total Honda Motor Co., Ltd. shareholders'

equity increased from 36.99% to 37.89% in 2014, with a growth rate of 6.42% is equivalent to

¥875,479 million. This suggests that the company has additional capital in business activities

aimed at expanding the market looking for more profits.

Conclusion: Thus, the allocation of capital in Honda Motor Co. Ltd. in 2014 have

markedly improved. Total liabilities tends to decrease. Total equity tends to increase. Shows

that companies are using their own money to invest in the business.

4.2.3. Analysis autonomy in financing activities.

To analyze the degree of independence and financial autonomy of the company, should

the criteria "funded ratio":

Coefficient sponsorship (%)

2014

37.89

2013

36.99

2012

37.26

Table 4.5: Table assess the level of financial independence.

Looking at the above table we can see, the numbers of indicators reflecting the degree of

financial independence from Honda in 2014 increased compared to 2013 and 2012 thus

demonstrates the level of financial independence of units has increased over the years. Thus,

the financial situation of the company is trending up. However, the amount of capital that the

company spent remains limited. This can assess the financial situation of the company is not

very convenient.

4.2.4. Analysis of solvency.

To assess the solvency of units, need to consider the relationship between solvency and

liquidity needs. Solvency of the unit include all properties that are capable unit at current prices

in payment at the time of study and are arranged in the order of rotation speed of capital.

Demand payment of the unit includes short-term liabilities, long term sorted in order of

payment terms.

2014

1.64

Generalized Ratio

2013

1.62

2012

1.62

Table 4.6: The list of general payments.

We see the overall solvency of the unit in 2014 increased compared to 2013 and 2012 at

the time of 2013 and 2012, the solvency Essential 1.62 times, 1.64 times the time in 2014. This

is a fundamental factor contributing to the financial stability of the unit. Ratio of overall units

in 2014 compared to 2013 increased from 1.62 to 1.64 with 0.02 pace of 1.2%. This growth

rate is small, but the unit also demonstrated the ability to pay the debts of the company is

gradually raised to make the financial situation of the unit more stable, positive impact to

business operations.

* Analysis of the short-term solvency.

To analyze the short-term solvency of the Vietnam Dairy Products Joint Stock Company, we

determine the reflection coefficient of solvency in the short term.

2014

Chỉ số hiện hành

1.93

2013

1.98

Chênh lệch

2012

±

%

(2014/2013)

1.93

-0.05

-2.75

Chênh lệch

±

%

(2013/2012)

0.05

2.83

Table 4.7: Table evaluate the short-term solvency.

Solvency coefficient of short-term debt decreased in 2013 compared to 2012 was 0.02,

1.52% speed reduction. Meanwhile, the 2014 ratio fell 0.08 short time, or 6.15% decrease

compared to 2013 units. Demonstrate progress has been made in improving the financial

situation. However, in both years, the solvency ratio of short-term debt is higher than 1 unit

demonstrates that there is sufficient short-term assets to pay short-term liabilities. From a shortterm payment situation we see on the solvency of short-term debt is relatively good unit.

4.3.1. The report analyzed the results of operations:

To control the operations and business performance, consider the fluctuation of the items

in the statement of earnings. We need to analyze and compare the rates and rate fluctuations

between the years of each indicator on report operating results. To report analyzes business

results in 2014 to compare the 2013 targets on reported operating results for the 2014 targets.

Table 4.8: A breakdown of reported operating results

Unit: Yen (millions)

Difference

Indicators

2014

2013

Net sales and other

operating revenue

11,842,451

9,877,947

7,948,095

1,964,504

19.89

1,929,852

24.28

8,761,083

7,345,162

5,919,633

1,415,921

19.28

1,425,529

24.08

1,696,957

1,427,705

1,277,280

269,252

18.86

150,425

11.78

634,130

560,270

519,818

73,860

13.18

40,452

7.78

11,092,170

9,333,137

7,716,731

1,759,033

18.85

1,616,406

20.95

750,281

544,810

231,364

205,471

37.71

313,446

135.48

-21,341

-55,919

26,039

34,578

-61.84

-81,958

-314.75

Income before income

taxes and equity in

income of affiliates

728,940

488,891

257,403

240,049

49.10

231,488

89.93

Income tax expense

252,662

178,976

135,735

73,686

41.17

43,241

31.86

Equity in income of

affiliates

132,471

82,723

100,406

49,748

60.14

-17,683

-17.61

Net income attributable

to noncontrolling

interests

-34,642

-25,489

-10,592

-9,153

35.91

-14,897

140.64

574,107

367,149

211,482

206,958

56.37

155,667

73.61

318.54

203.71

117.34

115

56.37

86

73.61

Cost of sales

Selling, general and

administrative

Research and

development

Operating costs and

expenses

Operating income

Other income

(expenses)

Net income

attributable to Honda

Motor Co., Ltd.

Basic net income

attributable to Honda

Motor Co., Ltd per

common share

2012

Difference

Values

2014/2013

%

Values

2013/2012

%

From the analysis shows:

- The total profits of the company increased ¥155,667 million equivalent to 73.61%

compared with the year 2012. By 2014, net income attributable to Honda Motor Co., Ltd. is

¥574,107 million rose 56.37%. Thus we can see that the net income attributable to Honda tends

to decrease.

- In recent years a number of economies are more volatile and more difficult very

particular peers, as well as general company announced losses. This number is impressive

result. Given that the company had an effective year. Achieving this result is likely due to better

cost management and focus on the product added value.

Specifically:

- Net sales and other operating revenues in 2013 increased by ¥1,929,852 million, an

increase of 24.28%. In 2014 revenue increased by 18.89% (¥11,842,451 million). This figure

shows that the company's revenue decreased while the amount of investment the company has

grown, so companies need to take measures to improve the financial situation at present.

- Net profit from business operations of the company increased by ¥205,471 million

equivalent to 37.71% compared with 2013, an increase of 135.48% compared to 2012.

- In the men's 2013 Profit before income taxes and equity in earnings of affiliates

increased ¥231,488 million equivalent to 89.93%.

- Earnings before income taxes and equity in earnings of affiliates increased ¥240,049

million equivalent to 49.10%.

Net sales : Yen

(millions)

Japan

North America

Europe

Asia

Other

FY2010

70,461

103,956

124,665

461,067

380,143

FY2011

70,244

96,664

103,890

577,669

439,727

FY2012

72,915

97,306

96,146

579,562

502,899

FY2013

72,949

112,176

86,424

667,473

400,527

FY2014

79,455

141,563

102,634

868,464

471,515

Table 4.9: Net sales table selling motorcycles.

Net sales : Yen

(millions)

Japan

North America

Europe

Asia

Other

FY2010

FY2011

FY2012

FY2013

FY2014

1,383,855

3,013,432

575,326

1,041,258

540,977

1,310,734

3,252,852

441,696

1,221,704

567,112

1,329,645

2,855,683

355,963

836,301

428,383

1,462,664

3,905,276

388,464

1,385,449

567,363

1,714,752

4,717,769

487,673

1,599,069

657,097

Table 4.10: Net sales table selling cars.

The increase in revenue was mainly due to the growth of automobiles and motorcycles:

Besides, the wide distribution network in the world carved with production facilities authorized

in the country has increased revenue by increasing the number of products and product quality

are more advanced day.

Cost of sales in absolute terms increased from ¥7,345,162 in 2013 to ¥8,761,083

million in 2014 equivalent to the rate of 19.28%.

Selling expenses and general manager in 2014 reached ¥1,696,957 million, equivalent

to 18.86% compared to 2013, this increase is still lower than the growth in revenue. Therefore,

to obtain 100 in revenue in 2014 spent less than the cost of sales. In other words businesses

save costs business more efficient.

Cost of research and development rose 13.18% or ¥73,860 million. This shows that the

company has invested in research and development to produce new products to meet market

demand and to compete with other competitors.

Income tax expenses increased by ¥73,686 million equivalent to 41.17% of the income

showed strong growth that the company is pleased the company is worth:

Equity in earnings of affiliates in 2014 reached ¥132,471 million, an increase of

¥49,748 million equivalent to 60.14%: Demonstrated that the company's branch operations

effectively.

4.3.2. Analysis of the cash flow statement:

Report cash flow is a useful source of information for assessing the ability to generate

cash, solvency or capital requirements of a business loan. Cash flow statement is a summary

table to answer the question "of corporate money comes from and how used, for what

purpose?" It also enables us back to why businesses are profitable that borrowers must pay

taxes or state bankruptcy is because there is no debt payments ...

Thus, the analysis of the cash flows of an enterprise is one of the important pillars for the

administrator is able to capture the true financial situation of the company. So the financial

situation of how Honda is reflected through the cash flow situation of the company in 2014.

Difference

Indicators

Cash flows from

operating

activities

Cash flows from

investing

activities

Free cash flow

2014

Difference

2013

2012

1,229,191

800,744

761,538

428,447

53.51

39,206

5.15

-1,708,744

-1,069,756

-673,069

-638,988

59.73

-396,687

58.94

-479,553

-269,012

88,469

-210,541

78.26

-357,481

-404.07

Vaulues

2014/2013

%

Vaulues

2013/2012

%

Cash flows from

financing

activities

Effect of

exchange rate

changes on cash

and cash

equivalents

Net change in

cash and cash

equivalents

Cash and cash

equivalents at

beginning of the

year

Cash and cash

equivalents at end

of the period

370,555

119,567

-68,230

250,988

209.91

187,797

-275.24

71,784

108,460

-52,150

-36,676

-33.82

160,610

-307.98

-37,214

-40,985

-31,911

3,771

-9.20

-9,074

28.44

1,206,128

1,247,113

1,279,024

-40,985

-3.29

-31,911

-2.49

1,168,914

1,206,128

1,247,113

-37,214

-3.09

-40,985

-3.29

Table 4.11: Reporting cash flows.

Based on the above table it is easy to see, first formed in terms of cash flow from

operations in 2014, the net cash flow from business operations and financial performance

remaining balance revenue expenditure respectively ¥428,447 million and ¥ 250,988 million

while net cash flow from investing activities was net revenue expenditure was ¥638,988

million shortage:

On the basis of the balance between revenue and expenditure of money, the amount of

net cash flow in 2014 -¥37,214 million, and net amount of cash flow in 2013 is - ¥40,985

million. In 2014 the company has expanded its production scale, and on this basis has grown

operate effectively.

Figure 3: Graph showing cash flows (2010-2014).

So on average in 2014, only the operations only produce business and financial

operations are excess payments during the investment activity, the deficiency payment.

However, the results still showed a positive sign and reasonable. Because, in the investment

stage facilities company has cash balance of production and business activities.

From table analysis Cash Flow Report shows that, of the cash flows Honda Company is

primarily generated from operating activities and financing activities

* In 2013, net cash flow from operating activities was ¥800,744 million, suggesting

business activity increases the amount of units.

- Cash flow from financing activities was ¥119,567 million.

- Cash flow from investing activities is ¥-1,069,756 million. Investment proved to reduce the

amount of units. Although this activity creates a huge amount of money but besides that the

amount paid is greater than the amount of money generated should be negative.

*In 2014, net cash flow from operating activities was ¥1,229,191 million, an increase of

¥428,447 million compared to 2013 with 53.51% relative reduction.

- Business activities have a positive cash flow. This is the sign of a healthy, optimistic about the

ability to secure money for production and business activities.

Thus, summary cash flow from operating activities provide basic information to assess

the ability to generate cash from operations Honda. The company has a healthy financial

situation, pay the debts, maintenance activities, pay dividends and undertake new investment

activities without external sources of finance.

- Cash flow from investing activities is ¥-1,708,744 million, an increase of ¥638,988 million

compared with 2013 increased by 59.73% relative.

Looking at the cash flow statement. We see the net flow of investment is ¥-1,708,744 million.

This is not necessarily a bad sign for production and business activities. On the other hand,

suppose if the net cash flows from investing activities positive (revenues> expenses) is not

necessarily good because, while the results of the proceeds from the sale of fixed assets and the

recovery of capital investments own more than the amount spent to expand investment, fixed

asset purchases and increased financial investment. In other words, this means a contraction in

investment activities.

- Net cash flow from financing activities was ¥370,555 million yen rose versus ¥250,988

million in 2013 to 209.91% of relative.

So in 2014 financial performance has brought a major source of revenue for the company.

Through analysis of the cash flows on, we see, Honda is a company that has potential

indeed. The company not only creates brackish i recorded in the profit, but the profit is actually

generated, reflected by positive net cash flow of the company during the year. Ability to

generate cash and pay the company are also appreciated. Mobilization policies of major

transport company is using its own internal resources, this reaffirms the company's financial

good health. Besides the company is also a policy of reasonable use of the investment process,

expand market share, increase product quality floor ... prestige in the market continue to hold a

leading position.

The above analysis shows that remittance flows through two in 2013, 2014 is consistent with

the characteristics of business of the Company Honda.

4.3.3. Analysis of the financial statements for the detection of financial risks.

To analyze the financial risks we first consider debt settlement risks affecting the production

and business operation of the unit. Debt Settlement risk occurs when not enough or businesses

can not afford to pay. Therefore, to analyze our payment risk analysis focus and ability to pay

its debts and short-term debt limit.

2014

2013

2012

Difference

±(2014/2013)

%

Difference

±(2013/2012)

%

Ratio of general

1.64

1.62

1.62

0.02

1.23

0

0.00

Ratio of shortterm

1.22

1.30

1.32

-0.08

-6.15

-0.02

-1.52

Table 4.12: Table payment risk analysis.

Ability to pay short-term debt and reduce the overall solvency of the unit in 2014

increased slightly compared with 2013, in 2012 but remained low, indicating the unit has been

made in the payment of debts make the financial situation of the financial units encouraging.

In addition, to detect financial risks, we consider the indicators reflecting the relationship

between accounts receivable compared with liabilities (H) of the unit.

The percentage of receivables

against payables

2014

2013

2012

34.89

33.07

32.52

Table 4.13: Table percentage of receivables versus payables.

This indicator at 3 years is less than 100% debt units proved more sellers than buyers of

debt.Thus, the debt situation of the unit positive impact to the financial performance of the unit.

4.3.4. Analysis of the relationship between the financial reporting.

Besides analyzing each financial reports, analyzing the relationship between the

financial statement analysts will comprehensively assess the financial situation of enterprises.

To analyze the relationship between the report we focus primarily on the analysis of

generalized business performance, effective use of long-term assets, efficient use of short-term

assets.

Net sales and other

operating revenue

11,842,451

9,877,947

7,948,095

1,964,504

19.89

1,929,852

24.28

Income before

income taxes and

equity in income of

affiliates

728,940

488,891

257,403

240,049

49.10

231,488

89.93

Net income

attributable to Honda

Motor Co., Ltd.

574,107

367,149

211,482

206,958

56.37

155,667

73.61

Total Honda Motor

Co., Ltd.

shareholders' equity

5,918,979

5,043,500

4,392,226

875,479

17.36

651,274

14.83

Return on Assets

(ROA)

3.9

2.9

1.8

1.00

34.48

1.10

61.11

Return on Sales

(ROS)

4.8

3.7

2.7

1.10

29.73

1.00

37.04

Return on Equity

(ROE)

10.5

7.8

4.8

2.70

34.62

3.00

62.50

Table 4.14: Table generalized analysis business performance.

4.3.5. Analysis of business performance generalizations.

* Coefficient of profit after tax to assets (ROA) was 0.29 in 2013, meaning that for

every 100 properties are at potentially lucrative copper is 29 higher than in 2012 is 18 copper

while the eastern profitability is much higher at 39 compared to 2 in 2012 and 201.

We see, ROA increased 61.11% compared with 2012 and a downward trend in 2014 is

34.48% with an increase. However this increase remained high efficiency demonstrated good

properties, such as factors contributing improve capital efficiency.

* Return on equity (ROE) of the Corporation in 2014 was 1.05. That is when the other

factors constant, a contract equity participation in production and business activities will

generate profits here at 1.05 a profit is very attractive for investors because this ratio is

relatively high, in 2013, a contract equity participation in a co-production of business activities

will be 0.78 in profit: 2014 compared to 2013 increased 0.27 this increase is due to two

reasons:

- The Company uses the asset effectiveness is demonstrated by the increase in asset turnover.

Asset Turnover (Round)

2014

0.76

2013

0.72

2012

0.67

Table 4.15: Asset Turnover.

- Maintain a good level of gross profit in difficult times and have policies to control

costs better through increased profit margin on sales.

Now that we see that the strength of the profitability of equity of the Company has

increased over 3 years is due to the profit after tax of the company and increase net revenue of

the Corporation is increased in accordance with the law, besides the equity ownership has

increased over the years which suggests that the company has funded quite good and effective

use.

In 2014 the economic situation, with major macroeconomic fluctuations and

unpredictable as hyperinflation, frozen credit markets, recession ... so many businesses,

including business activities in the same field has suffered huge profits decline. However, the

results of the Honda business in 2014 showed that the profitability of the company are very

impressive improvement compared to the same period last year. This shows that the assertion

of product quality, reputation, has helped Honda increase its competitive position, market share

of greater than other companies in the same industry.

4.4.

Financial strategy for the company Honda.

To assess the level of management, executive producer of a business enterprise, it is used as a

measure of production efficiency of the enterprise business. Production and business

effectiveness is evaluated on two angles: economic efficiency and social performance. Within

the scope of corporate governance, it is primarily interested in economic efficiency. This is an

economic category reflects the utilization of corporate resources to achieve the best results with

the most reasonable cost. Thus the economic resources especially funds of enterprises have a

huge impact on the efficiency of production and business enterprises. Therefore, improving the

efficiency of capital is required nature and often mandatory for businesses. Efficiency rating

which will help us to see the performance in general business management and in particular the

use of capital.

Above, we have analyzed each common traits, individual financial situation of Honda Motor

Company. From this analysis, partly to see the positive aspects and limitations exist. For the

positive side, the enterprise should continue to develop further, while the surface is limited to

strive to find remedies.

To survive was difficult to stand even more difficult. Now, the problem is now overcome the

difficulties incurred in the enterprise. These problems hinder the path of business development.

From that judgment, plus an understanding of the business situation, 8 group strongly suggest

some recommendations to the desired small contribution to the development of the whole

enterprise.

4.4.1. Measures to increase the efficiency of fixed capital.

Fixed asset management: production line layout reasonable, mining capacity and improve

operating efficiency of machinery, solving all the fixed assets no longer needed or outdated also

consistent with the scale of production to recover fixed capital investment more modern

machinery and equipment to improve product quality. Or put into rotation, added to liquid

assets to produce more business.

For effective use of fixed capital in production and business activities, often need to implement

measures to not only preserve but also to develop the fixed capital of the business after each

business cycle. The essence is to ensure monetary amounts of capital to the end of a cycle, with

the number of capital can now withdraw or extend the amount of capital that businesses spent

initially to purchase investment fixed assets at current prices.

Must appreciate the value of fixed assets, facilitate accurate reflection of the state of affairs of

fixed capital, to preserve capital. Timely adjustments to facilitate exactly calculation of

depreciation expense, not to lose WC.

Determining the right time to use the fixed assets to determine the appropriate level of

depreciation, not to lose capital and minimize adverse h¬uong image of intangible

amortization.

Improving the efficiency of fixed assets of the business is all about time and productivity.

Timely disposal of fixed assets are not needed or did h¬u damage, no excessive reserves of

fixed assets not needed.

Well done maintenance mode, repair, preventive fixed assets not to happen down of fixed

assets hu¬ tr¬uoc h¬u down time or unusual damage to stop production. In the case of fixed

assets to conduct major repairs to consider, carefully calculate its performance. That is,

considered between costs should spend the first new shopping t¬u fixed assets to make a

decision accordingly.

Enterprises must actively implement measures to prevent risks in the business to limit losses of

fixed capital due to the objective reasons nhu¬: property insurance, the financial reserve fund ...

4.4.2. Measures to increase the efficiency of working capital.

Through analysis of the use of working capital Honda Motor Company in recent years shows

the capital needs of the company is very large but regular working capital is not sufficient to

meet demand.

So that led to the company to raise outside capital to finance working capital needs. Working

capital deficiency caused major debt situation. To avoid this situation when the construction

company working capital levels should be based on the specific situation in tr¬uoc of a

construction company working capital norms consistent with the financial situation of

enterprises do not cause shortage of working capital. At the same time to build working capital

norms for each quarter, each month to plan production suitable not wasters in the period.

While the Company's working capital, the company still missing other objects are still

occupied, this is not reasonable. So the debt collection business in the future need of a resolute

d¬uoc. In addition, businesses should also consider the liabilities for each customer t¬uong. If

customers have low prestige, now wants to sell should not be too wide to avoid risk. For trade

credit policy th¬uong reasonable business need to assess your level of risk or reputation of the

client. Need to carefully evaluate the impact of policies sold subject to corporate profits.

To assess the level of risk can be found in the sale of products can now consider the aspects

nhu¬ prestige level of the customer, general financial condition of the company, the value of

the products used to guarantee credit. In general, for each policy sold subject to business need

careful assessment in accordance with the following main parameters:

- Number of products l¬uong d¬uoc expected consumption.

- Selling price.

- The additional costs incurred for increasing the debt.

- The discount accept.

- The average debt collection period for the debt.

- Predict the number of customer accounts receivable.

The remedies and limited customer accounts receivable:

- Create a good image for your business to meet customer demand for such products quality,

delivery on time ... from which customers can easily arise goodwill in their business

transactions.

- Reduced price for customers ordering in bulk, or early payment

- Reminders, urging customers to their debts to their business when they are due.

- Agreement with the payment if the material is not enough business to pay cash but with

materials stored in the warehouse, it helps firms solve a debt capital for inventory and helps

businesses their part to save costs when buying materials outside the business conditions are

common materials.

- If your debts are too many businesses that can not afford the payment, then we can use that

debt to contribute capital to the business.

- Check the level of credibility and solvency of their business prior to selling debt.

- For bad debts should use measures such as reducing and reschedule if the solvency of

troubled businesses, sold debt for the debt buying business, legal use tool.

- At the same time in the stage of working capital reserves also make efficient use of working

capital decreases. When determining production needs during the early years of the company

should determine the appropriate reserves and rapid liberation of reserve assets if there is

excess.