PHÁT TRIỂN MÔ HÌNH SỬ DỤNG THÀNH CÔNG HỆ THỐNG HOẠCH ĐỊNH NGUỒN LỰC DOANH NGHIỆP CHO CÁC CHUYÊN GIA KẾ TOÁN

Bạn đang xem bản rút gọn của tài liệu. Xem và tải ngay bản đầy đủ của tài liệu tại đây (5.04 MB, 270 trang )

MINISTRY OF EDUCATION AND TRAINING

UNIVERSITY OF ECONOMICS HO CHI MINH CITY

-----

Phan, Thi Bao Quyen

A DEVELOPMENT OF ENTERPRISE

RESOURCE PLANNING SUCCESS

MODEL FOR ACCOUNTING

PROFESSIONALS

A DOCTORAL THESIS

Ho Chi Minh City, 2020

MINISTRY OF EDUCATION AND TRAINING

UNIVERSITY OF ECONOMICS HO CHI MINH CITY

-----

Phan, Thi Bao Quyen

A DEVELOPMENT OF ENTERPRISE

RESOURCE PLANNING SUCCESS

MODEL FOR ACCOUNTING

PROFESSIONALS

Major: Accounting

Code: 9340301

A DOCTORAL THESIS

Supervisors:

1. Associate Professor, Dr. Vo, Van Nhi

2. Dr. Nguyen, Thi Kim Cuc

Ho Chi Minh City, 2020

i

STATEMENT OF AUTHENTICATION

I certify that any content in this thesis has not previously been submitted for a degree at this or

any other institution.

I also certify that the dissertation is prepared by me. Any help that I have received in my

research work has been acknowledged. In addition, I certify that all sources and literature

used are adequately indicated in the reference.

Phan Thi Bao Quyen

ii

ACKNOWLEDGEMENTS

The effort to complete this thesis would not have been possible without the contribution of a

number of persons and organizations. First and foremost, I would like to express my deepest

gratitude to my two supervisors, Associate Professor, Dr. Vo Van Nhi and Dr. Nguyen Thi

Kim Cuc for their support and guidance. Especially Associate Professor, Dr. Vo Van Nhi, my

principal supervisor, his encouragement keeps me going even through the most difficult

moments of this study.

I would like to offer my gratitude to University of Economics Ho Chi Minh City, and

acknowledge the supports I have received from the School of Accounting at University of

Economics Ho Chi Minh City. I would like to thank Associate Professor, Dr. Nguyen Xuan

Hung and Dao Tat Thang for facilitating me completing the PhD thesis on time.

I would like to thank my colleagues in Accounting Information System Division for their

encouragement during my PhD journey. I would like to give a special thank to Dr. Nguyen

Phuoc Bao An for providing me constructive feedback and making me trust myself that I am

capable to finish this stressful research project. I also would like to thank Dr. Nguyen Bich

Lien for her comments on system-use concept of the ERP success model for accounting

professionals, which is a motivation for discovering a more appropriate system-use concept in

the ERP ongoing context. In my daily work, I would like to thank Dr. Luong Duc Thuan, Dr.

Pham Tra Lam, Nguyen Quoc Trung and Nguyen Huu Binh for supporting me to perform

lecturing-tasks in order to facilitate my researching.

I am so grateful to Dr. Nguyen Thi Thu for her enthusiasm for my research-method-relatedqueries. I would like to acknowledge the advices and the comments on how to effectively

adopt the Smart-PLS software to analyze the collected data from Dr. Nguyen Phong Nguyen.

I really appreciate his experience of such a useful tool. I would like to thank the help of Dr.

Trinh Hiep Thien for his assistance in distinguishing between reflective and formative

constructs.

I also would like to thank Nguyen Thao Nguyen for her counseling on

confirmation factor analysis.

iii

My thanks also go to academics from UEH and informants from participant organizations that

have assisted me to complete the pre-testing, pilot testing and main survey, whose names

cannot be disclosed owning to confidentiality agreements.

I would like to thank my brothers and sisters, as well as my friends, in particular, Phan Quoc

Hieu, Dr. Pham Thanh Ha, Phan Quoc Lan, and Nguyen Thi Thu Nguyet. Their help, support,

and friendship keep me balance every up and down moment and make the completion of this

thesis more interesting and enjoyable instead of pressure only or sometimes boringness.

I give special thanks to my parents, especially my wonderful mom, who have always stayed

by me, encouraged me to pursue my academic career, as well as assisting me to take care my

children. Without their support and sacrifice, this work would have been stalled. For this

reason, this thesis is dedicated to both of you.

Last but not least, I would like to thank my husband and my little daughters. Your love,

support and continual understanding have made this adventure possible. Therefore, this thesis

is also dedicated to all of you.

iv

TABLE OF CONTENTS

STATEMENT OF AUTHENTICATION

I

ACKNOWLEDGEMENTS

II

TABLE OF CONTENTS

IV

ABBREVIATIONS

VIII

LIST OF TABLES

IX

LIST OF FIGURES

XI

ABSTRACT

XII

CHAPTER 1 INTRODUCTION

1

1.1 Chapter introduction

1.2 Background of research

1.3 Motivations for research

1.3.1 Motivation 1 - ERP research

1.3.2 Motivation 2 – Behavioral Accounting Research (BAR)

1.3.3 Combination of ERP research and Behavioral Accounting research (BAR)

1.4 Research objective

1.5 Research questions

1.6 Justification

1.7 Methodology

1.8 Research scope

1.9 Thesis structure

1.10 Chapter summary

1

1

2

2

5

9

11

12

14

15

15

16

18

CHAPTER 2 LITERATURE REVIEW

19

2.1 Chapter introduction

2.2 Enterprise Resource Planning

2.2.1 Defining ERP

2.2.2 Evolution of ERP

2.2.3 Advantages and disadvantages of ERP

2.2.4 The ERP lifecycle

2.3 ERP Success Models

2.3.1 Challenges of measuring ERP success

2.3.2 A summary of ERP Success Models from 1990 up to present

2.3.3 Issues with the existing ERP success studies

2.3.4 Differences between the current study and the eleven previous ESMs

2.3.5 Review of ERP success studies in Vietnam

2.4 Review of ‘rich construct(s)’ enabling to overcome unanswered validity-setting-related issues

2.5 Chapter summary

19

20

20

22

23

25

25

25

27

43

46

47

45

47

CHAPTER 3 CONCEPTUAL FRAMEWORK, CONSTRUCT CONCEPTUALIZATION AND HYPOTHESES

49

3.1 Chapter introduction

49

v

3.2 Theories used in the ESMAP

3.2.1 D&M IS success model (DeLone & McLean, 1992)

3.2.2 IS-continuance theory (Bhattacherjee, 2001)

3.2.3 Principle “fitness for use” (J. M. Juran, 1988)

3.2.4 How to combine three theories to form the ESMAP

3.3 Conceptual ESMAP, construct conceptualization and hypotheses

3.3.1 Conceptual ESMAP

3.3.2 Relationships among constructs of organizational-level impacts

3.3.3 Perceived qualities and benefits; and organizational-level impacts

3.4 Chapter summary

49

49

50

52

54

54

54

55

61

62

CHAPTER 4 RESEARCH METHODOLOGY

63

4.1 Chapter introduction

4.2 Research approach

4.2.1 The nature of the phenomenon being studied

4.2.2 Research approach selection

4.3 Philosophical worldview

4.4 Research design

4.4.1 Selecting the type of research method

4.4.2 Time horizons

4.5 Research method

4.5.1 Instrument design

4.5.2 Sample design

4.5.3 Data collection

4.6 Ethical considerations

4.7 Chapter summary

63

64

64

65

65

65

65

66

66

67

75

80

81

82

CHAPTER 5 DATA ANALYSIS

83

5.1 Chapter introduction

5.2 Step 1: Data preparation

5.2.1 Data screening and cleaning

5.2.2 Straight lining check

5.2.3 Testing for outliers

5.2.4 Bias Tests

5.2.5 Section summary

5.3 Step 2: Instrument preparation

5.3.1 Instrument reliability assessment

5.3.2 Instrument validity assessment

5.4 Step 3: Testing the ESMAP

5.4.1 Analysis technique selection

5.4.2 Measurement model assessment

5.4.3 Structural model assessment

5.5 Chapter summary

83

84

86

86

86

87

88

88

89

89

97

97

99

104

122

CHAPTER 6 DISCUSSION OF FINDINGS

124

6.1 Chapter introduction

6.2 Descriptive findings

6.3 An overview of the relationship between accountant performance and organizational

performance

6.3.1 Discussion on organizations’ perceptions of organizational performance

124

124

128

128

vi

6.3.2 Discussion on organizations’ perceptions of accountant performance

6.3.3 Discussion on direct impact of accountant performance on organizational performance

6.4 Use and its outcomes

6.4.1 Discussion on organizations’ perceptions of use

6.4.2 Discussion on appropriateness of effective use in the ERP context

6.4.3 Discussion on direct impact of effective use on accountant performance

6.4.4 Additional discussion on indirect impact of effective use on organizational performance

6.5 Satisfaction and its outcomes

6.5.1 Discussion on organizations’ perceptions of satisfaction

6.5.2 Discussion on direct impact of satisfaction on accountant performance

6.5.3 Additional discussion on direct and indirect impact of satisfaction on organizational

performance

6.6 System quality and its direct impacts on use and satisfaction

6.6.1 Discussion on organizations’ perceptions of system quality

6.6.2 Discussion on direct impact of system quality on use

6.6.3 Discussion on direct impact of system quality on satisfaction

6.7 Information quality and its direct impacts on use and satisfaction

6.7.1 Discussion on organizations’ perceptions of information quality

6.7.2 Discussion on direct impact of information quality on use

6.7.3 Discussion on direct impact of information quality on satisfaction

6.7.4 Discussion on the role of information quality in D&M IS success model (1992)

6.7.5 Discussion on the role of information quality in the ESMAP

6.8 Perceived accounting benefit and its outcomes

6.8.1 Discussion on organizations’ perceptions of perceived accounting benefit

6.8.2 Discussion on operationalization of perceived accounting benefit

6.8.3 Discussion on direct impact of perceived accounting benefit on use

6.8.4 Discussion on direct impact of perceived accounting benefit on satisfaction

6.8.5 Additional discussion on direct and indirect impacts of perceived accounting benefit on

accountant performance and organizational performance

6.9 Other advanced discussions on the ESMAP

6.9.1 Differences of the ESMAP by the length of ERP system

6.9.2 Differences of the ESMAP by organizational size

6.9.3 Differences of the ESMAP by ERP vendors

6.10 Chapter summary

130

131

131

131

132

133

133

134

134

135

CHAPTER 7 CONCLUSION

149

7.1 Chapter introduction

7.2 Research questions revisited

7.2.1 How is the ERP success model for accounting professionals formed in order to improve

accountant performance, which in turn enhances organizational performance?

7.2.2 How is the ERP success model for accounting professionals (ESMAP) validated?

7.3 Contributions of the study

7.3.1 Theoretical contributions

7.3.2 Practical contributions

7.4 Limitations of the study and area for further research

7.5 Delineations and further research

7.6 Final concluding remarks

149

149

LIST OF PAPERS

159

REFERENCE

160

135

136

136

137

137

138

138

138

139

139

139

140

140

141

143

144

144

146

146

147

147

148

150

150

151

151

155

155

156

157

vii

APPENDICES

183

Appendix 2.1 Eleven previous ERP success models

183

Appendix 4.1 Advantages of using survey method in the current study

190

Appendix 4.2 Identifying formative and reflective constructs

191

Appendix 4.3 Evidence in relation to the expert panel’s feedback on the preliminary questionnaire

193

Appendix 4.4 The original Part A of the preliminary questionnaire

195

Appendix 4.5 A summary of changes in Part B of the preliminary questionnaire after analyzing

feedbacks from the expert panel

195

Appendix 4.6 The questionnaire after pre-testing

196

Appendix 4.7 Questionnaire translation process in the current study

200

Appendix 4.8 List of interviewees and demographic information

201

Appendix 4.9 Pilot study responses from three target informants

202

Appendix 4.10 The Vietnamese questionnaire after pilot testing

203

Appendix 4.11 Bias issues consideration and how to minimize them

207

Appendix 4.12 Sample size Calculator v2.0 for Cronbach’s Alpha Test

210

Appendix 4.13 The result of calculating the minimize sample size by G*Power software

211

Appendix 4.14 Sample size recommendation in PLS-SEM for a Statistical Power 80% (Hair Jr et al.,

2014)

211

Appendix 4.15 A covering letter

212

Appendix 5.1 Summary of Deleted Cases

213

Appendix 5.2 Result of Outlier Testing

214

Appendix 5.3 Independent Sample T-test for Non-response Bias

219

Appendix 5.4 Total Variance Explained for Common Method Bias Test

224

Appendix 5.5 Development of the final sample

226

Appendix 5.6 Instrument reliability assessment

227

Appendix 5.7 Sample characteristics consideration

229

Appendix 5.8 Process of interpreting the factors

234

Appendix 5.9 EFA Test Results - Scales without modifications

235

Appendix 5.10 Summary after Factor Analysis

236

Appendix 5.11.1 Results of fit consideration of higher-factor instruments – PAB

237

Appendix 5.11.2 Results of fit consideration of higher-factor instruments - USE

238

Appendix 5.12 Cross-factor loadings

239

Appendix 5.13 Internal consistency and convergent validity results of the first order factor

“PAB_operational” after eliminating indicator PAB18

240

Appendix 5.14 Decision-making process for keeping or deleting formative indicators basing on outer

weight and outer loading Hair Jr et al. (2014)

241

Appendix 5.15 Results of alternative models analysis

242

Appendix 6.1 Demographic characteristics of surveyed companies

245

Appendix 6.2 Demography characteristics of ERP system

246

Appendix 6.3 Demographic characteristics of informants

247

Appendix 6.4 Comparing sample means

248

Appendix 6.5 Testing the D&M IS Success model (1992) without PAB

251

Appendix 7.1 Practical implications for ERP adoption organizatons’ stakeholders

252

viii

ABBREVIATIONS

AP

AVE

B2B

B2C

BAR

CB-SEM

CFA

CFM

CFOs

CR

CSF/ CSFs

D&M

EFA

ERP

ES

ESM/ ESMs

ESMAP

Ex_U

Extended _U

FMCG

HTMT

IQ

IS

IT

KMO

MRP

OP

PAB

PCA

PLS-MGA

PLS-SEM

SAT

SQ

UEH

VAF

VIF

Accountant Performance

Average Variance Extracted

Business To Business

Business To Customer

Behavioral Accounting Research

Covariance-Based Structural Equation Modeling

Confirmatory Factor Analysis

Common Factor Model

Chief Finance Officer(s)

Composite Reliability

Critical Success Factor(s)

Delone And Mclean

Exploratory Factor Analysis

Enterprise Resource Planning

Enterprise Systems

ERP Success Model(s)

ERP Success Model For Accounting Professionals

Extent Of Use

Extended Use

Fast Moving Consumer Goods

Heterotrait-Monotrait Ratio

Information Qualilty

Information System

Information Technology

Kaiser-Meyer-Olkin Test

Manufacturing Resource Planning

Ogrnizational Performance

Perceived Accounting Benefit

Principal Component Analysis

Partial Least Squares – Multi-group Analysis

Partial Least Squares - Structural Equation Modeling

Satisfaction

System Quality

University Of Economics Ho Chi Minh City

Variance Accounted For

Variance Inflation Factor

ix

LIST OF TABLES

Table 1.1: Rankings of the most mentioned ERP-related topics (Huang & Yasuda, 2016) ...................................... 3

Table 2.1: Evolution of ERP ..................................................................................................................................... 22

Table 2.2: Advantages of ERP (Mohammad A. Rashid et al., 2002) ....................................................................... 24

Table 2.3: Disadvantages of ERP (Mohammad A. Rashid et al., 2002) .................................................................. 24

Table 2.4: ERP lifecycle models .............................................................................................................................. 25

Table 2.5: Summary of ERP success models from 1990 to present ....................................................................... 31

Table 2.6: A summary of studies involving measuring ERP success in Vietnam .................................................... 43

Table 2.7: Summary of definitions and how to develop the conceptualization of PAB in ERP context ................ 46

Table 2.8: Advantages of the ESMAP ..................................................................................................................... 48

Table 3.1: Differences among the training, adoption and ongoing use contexts (adapted from Deng et al.

(2004)) ........................................................................................................................................................... 56

Table 4.1: Conceptualization of the constructs ...................................................................................................... 67

Table 4.2: Indicators of System Quality .................................................................................................................. 68

Table 4.3: Indicators of Information Quality .......................................................................................................... 68

Table 4.4: Indicators of Perceived Accounting Benefit .......................................................................................... 69

Table 4.5: Indicators of Use .................................................................................................................................... 69

Table 4.6: Indicators of Satisfaction ....................................................................................................................... 70

Table 4.7: Indicators of Accountant Performance ................................................................................................. 71

Table 4.8: Indicators of Organizational Performance ............................................................................................ 71

Table 4.9: The minimize sample size of the current study ..................................................................................... 79

Table 5.1: Summary of The Factor Analysis Appropriateness Criteria ................................................................... 91

Table 5.2: EFA Test Results - Refined scales ........................................................................................................... 92

Table 5.3: New conceptualization and operationalization of new factors extracted from EFA ............................ 94

Table 5.6: Internal consistency, indicator reliability and convergent validity analyses of the first-order

measurement model................................................................................................................................... 100

Table 5.7: Discriminant validity (Fornell and Lacker criterion)............................................................................. 102

Table 5.8: Discriminant validity (HTMT) ............................................................................................................... 102

Table 5.9: Internal consistency, and convergent validity of the second-order measurement model ................. 103

Table 5.10: Validity of formative second-order constructs .................................................................................. 104

Table 5.11: Collinearity assessment of the ESMAP .............................................................................................. 105

Table 5.12: Direct relationships for hypothesis testing ........................................................................................ 108

Table 5.13: Summary of results in terms of path coefficients, f 2 and q2 value .................................................... 110

Table 5.14: Results of total and specific indirect effects ...................................................................................... 111

Table 5.15: Direct effects including mediators in the ESMAP .............................................................................. 112

x

Table 5.16: VAF values of each mediator model .................................................................................................. 113

Table 5.17: Results of specific indirect effects ..................................................................................................... 114

Table 5.18: Results of PLS-MGA for ERP implementation and post-implementation organizations .................. 115

Table 5.19: Results of PLS-MGA for large-sized and small-and-medium-sized organizations ............................. 116

Table 5.20: Results of PLS-MGA for popular and non-popular-ERP-packages-adopted organizations ............... 116

Table 5.21: Results comparison among models ................................................................................................... 117

Table 5.22: Results of the adjusted R2 value between the ESMAP and the parsimonious model ...................... 119

Table 5.23: Impacts of omitting information quality to use ................................................................................ 120

Table 5.24: Impacts of omitting information quality to satisfaction ................................................................... 121

Table 5.25: A summary of significant total effects among constructs and significant difference of several paths

in the ESMAP............................................................................................................................................... 122

Table 6.1: Comparison of Variance Explained among three models ................................................................... 132

Table 6.2: Summary of PAB's operationalization ................................................................................................. 142

Table 6.3: Summary of the current PAB construct's advantages (in comparison with the original PAB of Kanellou

and Spathis (2013)) ..................................................................................................................................... 143

xi

LIST OF FIGURES

Figure 1.1: Different management software types adopted in organizations in Vietnam ...................................... 2

Figure 1.2: The number of publications on "ERP" in Google Scholar by year .......................................................... 3

Figure 1.3: Accounting value chain (Hunton, 2002) ................................................................................................ 7

Figure 1.4: Research question hierarchy ................................................................................................................ 13

Figure 1.5: A systematic procedure for designing the ESMAP ............................................................................... 18

Figure 2.1: A literature map identifying uniqueness and worth of the research topic .......................................... 20

Figure 2.2: Stand-alone applications' architecture (Loh & Koh, 2004) .................................................................. 21

Figure 2.3: ERP-integrated architecture (Loh & Koh, 2004) ................................................................................... 21

Figure 2.4: ERP applications market shares split by top 10 ERP vendors and others in 2016 ............................... 23

Figure 2.5: Categories of IS success (DeLone & McLean, 1992) ............................................................................. 45

Figure 3.1: D&M IS Success Model (DeLone and McLean, 1992) ........................................................................... 50

Figure 3.2: IS-continuance theory (Bhattacherjee, 2001) ...................................................................................... 51

Figure 3.3: The research model (the ESMAP) ......................................................................................................... 54

Figure 4.1: A research framework of John W. Creswell (2013) .............................................................................. 63

Figure 4.2: Location of VN (green) in ASEAN (dark grey) (Referenced from wiki website) ................................... 76

Figure 4.3: Different management software types adopted in organizations in Vietnam .................................... 80

Figure 5.1: Data analysis process of the study ....................................................................................................... 84

Figure 5.2: Data preparation process of the study ................................................................................................. 85

Figure 5.3: Instrument Preparation Process of the study ...................................................................................... 96

Figure 5.4: Process of testing the ESMAP ............................................................................................................... 98

Figure 5.5: Hypotheses Testing _ Bootstrapping Direct Effect Results ................................................................ 107

Figure 6.1: Effects of the length of ERP adoption ................................................................................................ 126

Figure 6.2: Effects of the organizational size ........................................................................................................ 127

Figure 6.3: Organizations' perceptions of the ESMAP's constructs by the adopted ERP package ...................... 128

Figure 6.4: Descriptive findings of organizational performance .......................................................................... 129

Figure 6.5: Impacts of ERP lifecycle phases on firms' organization performance (Ross & Vitale, 2000) ............. 129

Figure 6.6: Descriptive findings of accountant performance ............................................................................... 130

Figure 6.7: Descriptive findings of use ................................................................................................................. 131

Figure 6.8: Descriptive findings of satisfaction..................................................................................................... 134

Figure 6.9: Descriptive findings of system quality ................................................................................................ 136

Figure 6.10: Descriptive findings of information system ..................................................................................... 138

Figure 6.11: Descriptive findings of perceived accounting benefit ...................................................................... 141

xii

ABSTRACT

Enterprise Resource Planning (ERP) system is commercial software that automates and

integrates many or most of a firm’s business processes. It allows to access to integrated data

cross the entire enterprise according to real-time (Davenport, 1998). Therefore, ERP system is

expected to increase productivity via processes standardization, to improve decision-making

ability via information integration throughout the whole enterprise, to enhance cooperation

between organizational entities by connecting them smoothly, and the most important, to

maintain competitive advantage once these benefits are satisfied (Davenport, 1998). These

promises are possibly a close explanation of its increasing popularity. Namely, Fortune 500

companies are trusting ERP system1 and it is also a solution that large-sized organizations in

Vietnam select and adopt more growingly2.

Nevertheless, instead of achieving impressive benefits from their ERP systems, some firms

have faced difficulties in gaining the benefits they expected. Therefore, as suggested by

Markus and Tanis (2000), for both researcher and executives, one of the initial interestedquestions is whether investments in ERP will pay off. Several organizational-level

econometric studies conducted (M. C. Anderson, Banker, & Ravindran, 2003; Hitt, Wu, &

Zhou, 2002) give an answer that it is likely yes – on average. However, the impacts vary from

enterprise to enterprise, even from module to module (Nicolaou, 2004a) in which accountingrelated modules are in charge of changed-focuses. Kanellou and Spathis (2013) perform the

relevant literature and conclude that ERP implementation has a considerable impact on

accounting department of the business organizations. Hence, the executives’ next questions

are probably to be, how can I maximize the positive impacts on accounting department? Is

there some way to predict what the ultimate impacts of ERP systems on accounting

professionals will be in order to achieve a goal of enhancing organizational performance?

These questions are worth addressing. In attempting to do so, the author draws on D&M IS

success model (DeLone & McLean, 1992), IS-continuance theory (Bhattacherjee, 2001) and

the principle “fitness for use” (J. M. Juran, 1988) to develop the ERP success model for

accounting professionals in order to make them more productive, which in turn improves

performance of implemented organizations. The theoretical and empirical results indicate that

organizational performance is, indeed, influenced by the extent to which accounting experts

effectively utilize ERP systems in the adoption and ongoing context.

1

2

This information is quoted from website />This information is quoted from Vietnamese E-commerce Indicator Report in 2018.

xiii

This study makes an original contribution to both of theory and practice through forming and

validating the ERP success model for accounting professionals only. In a little more detail, it

provides empirical evidence regarding Hunton’s accounting value chain (2002). In addition, it

discovers and proves effective use as the most appropriate system-use concept so far.

Moreover, it makes an effort to investigate outcomes of accounting benefits perceived from

ERP system, which related-studies are much further under-researched. Last but not least, the

research provides valuable implications for organization management on how they can

successfully manage accounting department as well as accounting professionals in an attempt

to maximize ERP’s impacts on organizational performance, which executives have paid much

attention to for recent years but have not yet found out the answer so far.

Key words: ERP success model, accounting professionals, perceived accounting benefits,

system use, the principle "fitness for use"

1

CHAPTER 1

INTRODUCTION

1.1 Chapter introduction

The purposes of this chapter are to describe a broad overview of the research, generally

present methodology, and introduce forthcoming chapters. This chapter begins with research

background, and moves on a discussion on two main motivations for research, which focus on

explanation what research topic is and why to choose it. Identifying research topic is very

important as it allows limiting the scope of reviewing a literature. The research objective and

research questions are then addressed in the third and forth part of this chapter. Next, section

five of this chapter represents research justification to make clarify the significance of the

study. Subsequently, research methodology is outlined to enable to image how to conduct the

whole dissertation, and followed by research scope. Finally, the thesis structure will be

proposed, providing description of the six forthcoming chapters of this thesis.

1.2 Background of research

Enterprise Resource Planning (ERP) system is one of the most popular forms of IT for

businesses at present. Deriving from efforts to rationalize lead times and possession stock

costs, the 80’s manufacturing resource planning (MRP II) is developed into ERP system

considered as the standard that integrates business processes throughout the organization,

which in turn enhances operational efficiency (Akkermans, Bogerd, Yücesan, & Van

Wassenhove, 2003; Davenport, 1998). Callaway (1999) states that the ERP system promises

to achieve benefits in both tangible (e.g., reduced personnel, inventory, IT and procurement,

transportation, and logistic costs; improved cash flow management, revenue and profits) and

intangible (e.g., increased visibility of corporate data, speed of decision making, and control

over global business operations; improved customer responsiveness and business processes)

manner.

Such those benefits push business organizations towards adopting the ERP systems

(Davenport, 1998; Ifinedo, Udo, & Ifinedo, 2010; Vincent A. Mabert, Soni, &

Venkataramanan, 2003). This has been proved by tremendous expansion of the worldwide

ERP applications market for the last ten years. Its revenue, about $38 billion in 2008 (Ifinedo,

Rapp, Ifinedo, & Sundberg, 2010), has grown more than twice to approach nearly $82.2

2

billion in 2016. This ERP applications market is expected to continuously increase and reach

$84.7 billion by 20213.

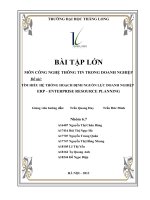

Being consistent with the trend, in Vietnam, E-Commerce Indicator Report in 2017 also

indicates that the number of organizations adopting ERP system has been more increased in

2016.

Human

resource

management

Accounting/

Financial

software

SCM

CRM

ERP

Figure 1.1: Different management software types adopted in organizations in Vietnam

(Source: Vietnamese E-commerce Indicator Report in 2017)

As such, this study is conducted in the context, which the ERP system has already been one of

the most popular business-management-applications in organizations all over the world and

begins to be increasingly adopted in Vietnam.

1.3 Motivations for research

1.3.1 Motivation 1 - ERP research

With respect to a boom in ERP-adopted business organizations, research in the ERP has also

increased over the past years. To acquire how the growth of publications about ERP is, the

Google Scholar database is scanned for the term “Enterprise Resource Planning” in the period

1990-2016. The results of this searching are summarized in following bibliometric4 graph (see

Figure 1.2). This graph reveals the growing interest in ERP over the past 26 years.

Accordingly, ERP (although a little decrease) is still a prominent field in the research

community, with about 6000 search results on average in the 2009-2016 period (Google

2017).

3

These figures are quoted from the Allert Pang’s report (December 1st 2017) that is posed on website Apps

Run The World. Retrieved September 18th 2018 from />4

Bibliometrics is statistical analysis of bibliographic data; commonly focusing on citation analysis of research

output and publications, i.e. how many times research outputs and publications are being cited (Leeds University

Library 2017)

3

Figure 1.2: The number of publications on "ERP" in Google Scholar by year (Source: by author)

Huang and Yasuda (2016) conduct a comprehensive review of literature survey articles on the

ERP to highlight the current research status of this field. As a result, they summarize the most

mentioned ERP-related topics as follows:

Table 1.1: Rankings of the most mentioned ERP-related topics (Huang & Yasuda, 2016)

No.

1

2

3

4

5

6

7

8

9

10

The most mentioned ERP-related topics

New emerging ERP technologies

Critical success/ failure factors

Business process reengineering

Real benefits

System/ organization performance evaluation

User satisfaction

ERP selection criteria

ERP impacts

Change management

Implementation strategy

Among ten topics above, ERP critical success factors (CSFs) has been the most prolific area

in early ERP research (Grabski, Leech, & Schmidt, 2011). The reason of this may be that ERP

is very expensive, complex system, impacts the entire organization, and if it fails, it seems

likely to contribute to the failure of the firm itself (J. Scott, 1999). Moreover, many adopting

enterprises realize that the deployment of such systems is not as effective as expected (E. T.

G. Wang, Shih, Jiang, & Klein, 2008). Critical success factors (CSF) have thus constituted

few things that must go well to ensure success of an organization (Boynton & Zmud, 1984).

CSF is investigated to identify essential areas of concern and provides measures that would

aid in managing those areas (Boynton & Zmud, 1984). The CSF researches have typically

addressed several different issues. In most cases, typical CSF studies have consistently

identified a set of core factors critical to the success of ERP implementations including top

management support, the implementation team, organization-wide commitment to the system,

4

and fit between the ERP systems and the firm (Finney & Corbett, 2007; Hong & Kim, 2002;

Murray & Coffin, 2001; Ross & Vitale, 2000; J. E. Scott & Vessey, 2000; Somers & Nelson,

2001; Somers & Nelson, 2003; Stefanou, 2000). In other cases, some papers have found that

firm size is also an important factor related to ERP implementation success (Bernroider &

Koch, 2001; Buonanno et al., 2005; Vincent A. Mabert et al., 2003; Muscatello, 2003; Snider,

da Silveira, & Balakrishnan, 2009).

Alternatively, rather than focusing on identifying the factors critical for success in

implementing ERP system, the few researchers are interested in building ERP success models

as untypical CSF studies. For instance, H.-Y. Lin, Hsu, and Ting (2006) develop an ERP

success model upon the DeLone and McLean’s (1992, 2003) information system success

model. Lin et al.’s (2006) model relates the individual impact to balanced scorecard measures

(i.e., financial effectiveness, customer effectiveness, internal business effectiveness, and

innovation and learning effectiveness). They demonstrate that the success of any ERP system

may be predicted by integration of the information system success model and balance

scorecard constructs. Specifically, they suggest that the adoption of balance scorecard criteria

will allow firms to more easily assess impacts of the ERP system is either positive or negative

as well as to more effectively manage the ERP system implementation.

ERP CSFs research is crucial; however, quite mature for a certain period of time; therefore, a

question is whether there still have the interesting research opportunities for ERP researchers.

Drawing on recent relevant literature, Mukti and Rawani (2016) as well as Grabski et al.

(2011) assert that there exists a paucity of ERP success model research. Thus, this study is

expected to increase insight regarding such an area. Another reason of choosing ERP success

model to study in place of investigating single critical success factors is due to its

advantages5. First, the ERP system causes complex and challenging tasks, and there are many

integrated factors influencing the level of success, therefore identifying primary factors

running organizational performance under a whole model is more appropriate. Second, the

model forces researchers to be explicit about the way the problem is perceived. Thus, there is

less room for sloppy or confused thinking when modeling. The act of systematically

considering the impact of one variable on another forces researchers to make their logic more

consistent when thinking about a problem. Third, model is effective and efficient way of

organizing researchers’ knowledge about a problem of interest. Hypotheses investigated in

model will expand their knowledge about the phenomena. Finally, model provides a safe and

5

The last three reasons are quoted by J. W. Jones, Steffy, and Bray (1991).

5

economical way of testing relationships as it allows simulating the effect of making a change

in one variable on other variables without actually making the change.

Finney and Corbett (2007) lament the fact that most of recent ERP CSF research (both typical

and untypical CSF type) has generally taken from a macro perspective or a view of multiple

top mangers, the perspectives of key or single stakeholders are often missing. This proves that

CSF research potentially still lies in either micro-level or target-level approaches. Likewise,

Grabski et al. (2011) suggest that ERP research has yet to sufficiently investigate some issues

such as how ERP influences stakeholders in accordance with stakeholders’ insights; or

whether stakeholders’ performance can be effectively improved in organizations adopting

ERP; or even whether the perceptions of stakeholders on the ERP system can enhance the

organizational performance of adopting enterprises. To put it in other way, to comprehend

positive impacts of the ERP system on stakeholders, a question is whether there is a model

guiding stakeholders how to adopt ERP successfully in order to contribute to increasing

organizational performance from stakeholders’ perspectives themselves.

For these reasons, it could be concluded that in terms of ERP research, a call for developing a

model measuring ERP success from stakeholders’ perspective has been established for recent

years.

1.3.2 Motivation 2 – Behavioral Accounting Research (BAR)

Behavioral accounting research (BAR) or behavioral research in accounting is defined as the

study of accounting professionals’ behavior or non-accountants’ behavior influenced by

accounting functions, and/or report system, and/or creating accounting information (Hofstedt

& Kinard, 1970).

Since the late twentieth century, BAR have drawn increasing attention from accounting

researchers, academics and international community (Nowak, 2016 ). In the early stage of

BAR, Birnberg and Shields (1989, pp. 41-61) extract five accounting-related schools of

behavioral research, namely:

(1) Managerial control – designing and implementing control system for staffs and firm;

(2) Accounting information processing – guiding users how to gather, process, store, and

create accounting information;

(3) Accounting information system design – concerning behavioral issues when conducting

to design information system of business organizations.

(4) Auditing-related-issues research – i.e., decision-making behavior of auditors

(5) Organizational-subjectivity-issues research – identifying the nature and interpretation of

social interactions in ideographic (as opposed to nomothetic) manner.

6

Out of these five schools of accounting behavioral research, Birnberg and Shields (1989) also

mention a few behavioral researches related to accountants, which are called the studies of

accountants. Because of their shortage, they have not yet constituted the sixth school of

behavioral research in accounting. Likewise, Sorensen (1990) determines that the a school of

‘study of accountants’, indeed, exists however its status is alarming.

Recently, Tin, Agustina, and Meyliana (2017) conduct a comprehensive review to obtain a

clearer picture and more extensive knowledge about direction and development in behavioral

aspects of accounting. Accordingly, behavioral accounting research scopes from 2005 to 2014

are classified into seven schools as follows:

(1) Topics discuss the effect of human behavior on the design, construction, and use of the

accounting system (10.74%)

(2) Topics discuss the effect of accounting system on human behavior (13.22%)

(3) Topics discuss the method/ strategy to alter human behavior (29.75%)

(4) Topics discuss the handling of human that can affect subject’s behavior (27.28%)

(5) Topics discuss the research methodology associated with a behavioral aspect of

accounting, such as examining measures, developing measures, and variable construct

dimension towards human behavior examination (9.09%)

(6) Topics discuss building a model in accounting professions (3.3%)

(7) Topics discuss the use of theory to analyze human behavior in accounting (7.43%)

Given these related literature reviews of behavioral research in accounting, it is obvious that

research directions of behavioral accounting are broader developing although the priority to

each school at each moment is dramatically different. Notably, among such schools, study of

accountants is, indeed, more growingly concerned. This school, from being charged of the

few studies in 1989 (Birnberg & Shields, 1989), has been considered as a part of an

individual, independent group (10.74%) in recent years (Tin et al., 2017). The evidence points

to the fact that a call for the ‘study of accountants’ is real and vital.

Not only choosing study of accountants as a response to its call, this study intends to focus on

it because of the increasingly dramatic change of accountants’ roles and functions in ERP

environment. For example, Sayed (2006) emphasizes that the traditional accounting role in

IS-adopted organizations is declining. However, rather than a threat, he provides evidence

that accountants exploit the ERP system as an occasion where their skills and their accounting

knowledge are represented. Likewise, Newman and Westrup (2005) indicate that accountants

should be considered as subjects that need to be paid more attention to as the relationship of

accountants and the ERP system has become more increasingly intertwined. This relationship

7

is confirmed via the findings of their survey in which about 83% of those who have some

experience of the ERP system choose the statement ‘the ERP system have positive effects on

management accountants’ in comparison with a total of 55% interviewees agree with the

statement ‘the ERP system have positive effect on organizational performance’ when being

required to give opinions about perceived effects of the ERP systems on organizations and on

management accountants. According to these statistics, there is no denial that users who

experience the ERP system easily recognize the impacts of ERP system on management

accountants, rather than on organizational performance. Moreover, their respondents (senior

accountants) concede that the ERP system is as a positive development enabling them to be

more focused on financial management and less on bookkeeping aspects. Furthermore, rather

than being changed their role by the ERP system only, accountants, in contrast, also influence

the design of ERP systems. For example, in ERP pre-implementation stage, when questioning

vendors about features that are supported by their packages, the focus of questions is often on

whether certain techniques such ABC and the balanced score card could be supported by their

product (Newman & Westrup, 2005).

Another reason explaining why a school of ‘study of accountant’ is chosen in this thesis is due

to accountants’ contributions to organization value in business organizations adopting IS,

especially ERP system. Drawing on Porter’s value chain and Elliott’s information value

chain, J. E. Hunton (2002) proposes the accounting value chain (shown in Figure 1.3) which

illuminates how accountants can add value to business organizations in today’s global

information and communication technology environment.

Figure 1.3: Accounting value chain (Hunton, 2002)

8

Figure 1.3 reflects that the accounting value chain includes three-value levels ranging from

low to high level in the IS context. On its low-value side, accountants have no longer

opportunities to add incremental value to the traditional functions relating to identify,

measure, and record accounting transactions owing to IS’s predictability, and automaticability. The following phase of such a chain focuses on translating data into information that

makes sense. In a little more detail, in routine work, recording and processing accounting

transactions as well as creating previous formatted-information are conducted automatically.

Reliable IS controls relating to accounting are a guarantee of the integrity of such systems. As

such, accountants’ contributions in this phase are also not high. It can be easily realized that,

in the IS context, the more increasingly the accounting functions and tasks can be performed

by IS, the lower the accountants can contribute to benefits to enterprises. Therefore, the

significant contributions of accountants focus on the side that IT just assists instead of

performing accountants’ tasks. Here are some of outstanding values that accountants can

create in IS adopting organizations:

(1) Disseminating business knowledge: Information system provides functions and features

which allow accountants to generate, manage, integrate business knowledge and

disseminate such knowledge to inside and outside users of the organizations. Under the

viewpoint of Elliott (2001), a capability of knowledge leveraging makes accounting

professionals distinguish rather than different types of staffs.

(2) Developing externalities: Merging e-commerce and supply chains into organization

operations likely leads to appearance of externalities, which in turn creates new works

for accountants. For example, they need to monitor, control the flows of information

and protect the privacy, confidentiality and security rights of related parties. These

requirements undoubtedly put pressure on accounting experts, but, on the other hand,

propose opportunities for them to add more value to their companies.

(3) Providing assurance: Not only adding value impossibly-replaced to organizations,

accounting professionals also provide assurance for managers, investors, and societies

via auditor’s opinion regarding the fairness on and off financial reporting.

(4) Internal value of accounting systems: Drawing on data integration feature of some IS

(especially ERP system), accountants conduct to process data, and create useful

decision-making information more quickly, reliably and relevantly.

To sum up, this thesis focuses on “study of accountants” due to its increasing concern in BAR

literature; the more growingly intertwined relationship between accountants and ERP system;

and their valuable contributions in IS-adopting business organizations.

9

1.3.3 Combination of ERP research and Behavioral Accounting research (BAR)

Combination of ERP research and BAR is essential and timely because ERP is a

transformative force on the accounting. In reality, because of its accounting benefits, ERP

requires accounting expertises to change their role in order to make broader contribution to

the company, such as reporting on non-financial measures, auditing information systems,

implementing management controls within information systems, and providing management

consulting services (Grabski et al., 2011). Therefore, the thesis will combine ERP CSFs

research with the study of accountants.

Given research gaps related ERP research and BAR, a research topic is formulated. That is to

discover how to assess ERP success for accounting professionals from accounting

professionals’ perspective themselves, in simple terms, developing an ERP success model for

accounting professionals (ESMAP).

It is worth noting that there are virtually no researches of the ESMAP, thus, it is considered as

the first and unique study up to now in an effort to better understand ERP system-related

drivers leading improvement in organizational performance toward a point of accounting

experts’ view.

Drucker (2018) once said: “What you measure is what you get.” “Ensure that every measure

of performance is pertinent to be achievement of a goal or value of your organization.

Otherwise, you risk misdirecting your organization.” Accordingly, give the relatively few

studies on the development of ERP success model (ESM) (G. Gable, Sedera, & Chan, 2003;

Ifinedo, 2006; H.-Y. Lin et al., 2006; Smyth, 2001), two broad problems are identified: first,

the validity of ESM design and second, target setting in ESM design. These are also primary

concerns in developing the ESMAP.

Validity issue of the ESMAP design

The first problem in this line of research relates to the validity of the ESMAP. Being adapted

from Ittner and Larcker (2001), validity in this study is defined as ‘the extent to which a

model succeeds in capturing what it is supposed to capture’. Accordingly, there are two

questions that need to be considered when designing a model: what is supposed to be

captured? and how can a framework be designed to successfully capture this?

In the context of this study, the success of adopting the ERP system of accounting experts is

what supposed to be captured. Therefore, the remaining question is how a framework can be

designed to successfully capture the ERP success for accounting professionals.