Improving competitiveness of Petrolimex Joint-Stock Insurance Company = Nâng cao năng lực cạnh tranh công ty Cổ phần Bảo Hiểm Petrolimex

Bạn đang xem bản rút gọn của tài liệu. Xem và tải ngay bản đầy đủ của tài liệu tại đây (1.36 MB, 119 trang )

vietnam national university, HANOI

school of business

Do Thi Mai

IMPROVING COMPETITIVENESS of

PETROLIMEX JOINT- STOCK INSURANCE COMPANY

Major: Business Administration

Code: 60 34 05

Master of business administration thesis

Supervisor: Dr. Tran Phuong Lan

Hanoi - 2011

vi

TABLE OF CONTENT

ACKNOWLEDGMENTS i

ABSTRACT ii

TÓM TẮT iv

TABLE OF CONTENT vi

LIST OF TABLES vii

LIST OF FIGURES ix

LIST OF ABRREVIATION x

INTRODUCTION 1

1. The problem 1

2. Objectives 1

3. Research Questions 1

4. Scope of work 2

5. Methodology and data sources 2

6. Significance and expected results 2

7. Limitations 3

8. Thesis Structure 3

CHAPTER 1: THEORETICAL FOUNDATIONS 4

1.1 Definition of competitiveness 4

1.2 Sources of competitiveness 5

1.3 Models to assess and analyze industrial competitive environment 6

1.4. Models to analyze firm competitiveness 14

CHAPTER 2: RESEARCH AND ANALYSIS APPLICATION OF MODELS TO

ANALYZE PJICO’s COMPETITIVENESS 16

2.1 Overview of non-life insurance industry in general and in Vietnam 16

2.1.1. Non-life insurance industry in recent years 16

2.1.2 Non-life insurance industry in Vietnam 20

2.1.3 Key success factors in non-life insurance industry 25

2.1.4. Factors affecting non-life insurance enterprise’s competitiveness 27

2.2. Overview of PJICO 29

vii

2.2.1. Introduction of PJICO 29

2.2.2. PJICO’s business activities 33

Unit: VND billion 35

2.3. Application of models to analyze PJICO’s competitiveness 39

2.3.1. Application of PEST & Five Forces models to analyze factors affecting

PJICO’s competitiveness 39

2.3.2. Application of Value Chain model to analyze and evaluate PJICO’s

competitiveness 51

2.3.3. PJICO’s competitive position in comparison with its main competitors 76

CHAPTER 3: CONCLUSIONS AND RECOMMENDATIONS 80

3.1. Conclusion of PJICO’s Competitiveness 80

3.1.1. Summary from internal analysis and competitiveness comparison 80

3.1.2. Assess to the real PJICO’s strengths & weaknesses – the core

compentencies 85

3.2. Solutions for PJICO to strengthen its competitiveness & to achieve its

objectives 89

3.2.1. PJICO’s strategic vision and objectives 89

3.2.2. Solutions for improving PJICO’s competitiveness until 2017 90

3.3. Recommendations 106

3.3.1. Recommendations to Government 106

3.3.2. Recommendations to Association of Vietnamese Insurers 107

3.3.3. Recommendations to PJICO 108

REFERENCES 109

APPENDICES 111

LIST OF TABLES

Table 1.1: Selected connotations of firm level competitiveness: 5

Table 1.2: The five forces that shape industry competition of Michael Porter 9

viii

Table 2.1: Real growth rate of Industrialized and Emerging markets (1980 – 2009) 17

Table2.2: Real growth rate of insurance market of developing countries (1980 -

2010) 18

Table 2.3: Asia Pacific Non-life markets at a glance, 2008 - 2010 19

Table2.4: Vietnam’s top 10 non-life insurance market share 2005-2010 21

Table2.5: Non-life insurance premium income and premium growth 2004-2010 21

Table2.6: Premium and Loss by class in 2010 23

Table 2.7: Gross Premium Income by Type of Insurance 2007-2010 38

Table 2.8: Vietnam’s non-life insurance market shares 2005- 2010 47

Table 2.9: Conclusion of Environment analysis – Chances and Challenges 51

Table 2.10: Labor Force of PJICO 2006-2010 69

Table 2.11: Statistics of Training Courses 2007-2010 70

Table 2.12: Some financial criteria of PJICO 2007-2010 73

Table 2.13: Competitiveness Comparison 77

Table 3.1: Identification of Sustainable Competitive Advantages - Strengths 85

Table 3.2: Identification of Sustainable Competitive Advantages – Weaknesses 86

Table 3.3: The real PJICO’s strengths and weaknesses – Core competencies 88

Table 3.4: Possible solutions and actions 91

ix

LIST OF FIGURES

Figure 1.1: Value chain 14

Figure 2.1: Market premium and loss 2006-2010 22

Figure 2.2: Non-life insurance premiums by business lines 23

Figure 2.3: Market share of Non-life Insruance Companies 2010 31

Figure 2.4: Insurance Premium Income 2005-2010 35

Figure 2.5: PJICO’s Product Portfolio in 2010 36

Figure 2.6: Vietnam’s GDP 42

Figure 2.7: Vietnam’s savings and current account balance (in % of GDP) 43

Figure 2.8: Vietnam’s inflation and exchange rate 43

Figure 2.9: Some Vietnam’s economic figures 44

Figure 2.10: Value chain of PJICO ……………………………………………… 52

Figure 2.11: Process of new product design 53

Figure 2.12: Underwriting process 59

Figure 2.13: PJICO’s process of reinsurance 62

Figure 2.14: Survey process for non-life insurance products of PJICO 64

Figure 2.15: Claims handling process for non-life insurance products of PJICO 65

x

LIST OF ABRREVIATION

PJICO

Petrolimex joint-stock insurance company

SWOT

Strengths, Weaknesses, Opportunities, Threat

PEST

Political, Economic, Social, Technological

R & D

Research & Development

SCIC

State Capital Investment Corporation

CEO

Chief Executive Officer

GDP

Gross Domestic Price

IT

Informatics Technology

1

INTRODUCTION

1. The problem

Vietnamese non-life insurance market has been experiencing a challenging,

struggling as well as fast-developing stage. Going along with this context, each and

every participant in this market needs to focus more on their real competitiveness to

achieve further growth and sustainability; and PJICO is one of these players.

Moreover, until now, there has not been a complete and thorough analysis on

PJICO’s competitiveness and the ways to improve the real competitiveness.

Therefore, the thesis is born to conduct analyses on PJICO’s competitiveness and

suggest possible solutions to strengthen its competitiveness in order to stand and

develop in Vietnamese non-life insurance market in the future.

2. Objectives

The objectives of this study can be listed as follows:

Give the overview on concept of competitiveness

Provide some analyses on macro and industry environment of insurance

market

Conduct a thorough study on PJICO’s competitiveness

Recommend the possible ways to improve the current competitiveness so

as to help PJICO be stable and progressive in the insurance market.

3. Research Questions

Based on the problem and objectives listed above, some research questions are

given and discussed:

a. What is competitiveness?

b. Method and process to analyze competitiveness of a firm?

c. The way to conduct macro and industry environment analysis of

insurance market?

2

d. The way to conduct internal environment analysis of an insurance

company?

e. What are suggestive solutions to improve the competitiveness of PJICO

to the year 2017?

Answering these above questions shall help the author fulfill and reach the

objectives which the thesis are required to achieve.

4. Scope of work

In terms of theory, the thesis focuses on the concept of competitiveness, macro and

industry environment analysis, and internal environment analysis of an enterprise.

In terms of practice, the thesis focuses on reviewing the current insurance market in

Vietnam, analyzing the external and internal environment of insurance market in

order to assess the competitiveness of PJICO, and giving recommendations on

possible solutions to improve its competitiveness to the year 2017.

5. Methodology and data sources

This study uses the descriptive method for analysis through a specific case study of

PJICO in the context of present Vietnam insurance market.

The data are sourced through two ways:

a. Secondary data are collected from research of books, websites, teaching

notes, reports, magazines and newspaper, and other available documents.

b. The primary data are collected chiefly through deep interviews with

PJICO’s as well as partners’, other players’ managers, key staffs, and

their customers. The details of primary data are shown in analyses in

Chapter 2 and Chapter 3; the list of interviewees and the list of

questionnaires are shown in the Appendix 1 and 2.

6. Significance and expected results

By scanning the specific theory on competitiveness and analyzing the impacts of

business environment of non-life insurance market, the study helps PJICO in giving

suggestive solutions to improve its competitiveness to the year 2017.

3

Therefore, this methodology, information and analysis can be applied for other

companies or other insurance companies or for the PJICO itself in other stages of

development.

7. Limitations

This thesis is conducted in narrowed scope of insurance market and the applications

to PJICO in certain period to the near future until 2017. Thus, it may not wholly

express and reflect the business environment as the whole and in other periods.

8. Thesis Structure

The study includes four parts as below:

a. Introduction

b. Chapter 1: Literature review and overview of non-life insurance market

c. Chapter 2: Research and applications of models to analyze PJICO’s

competitiveness

d. Chapter 3: Conclusions and recommendations

4

CHAPTER 1: THEORETICAL FOUNDATIONS

Day by day, firms have been facing increasing numbers of challenges, changes and

competitors. Indeed, being successful is requiring new perspective and practice on

competitiveness.

1.1 Definition of competitiveness

In spite of its significance, the concept and definition of competitiveness is widely

controversial. Up till now, there has been no generally accepted definition of

competitiveness as well as no mutually accepted definition to explain it. In the

simplest terms, competitiveness is the ability to compete. It has become the name of

the game where economic strength of a country or an industry or a firm is described

with respect to its rivals in the global market economy, in which goods and

resources can move freely throughout territorial borders.

In other terms, competitiveness is a broad concept. According to Beckley, “A firm

is competitive if it can produce and services of superior quality and lower costs than

its domestic and international competitors. Competitive is synonymous with a

firm’s long run profit performance and its ability to compensate its employees and

provide superior returns to its owners”. The Organization of Economic Cooperation

and Development (OECD) defines competitiveness as “the ability of companies,

industries, regions, nations and supranational regions to generate, while being and

remaining exposed to international competition, relatively high factor income and

factor employment levels on a sustainable basis.” Whereas, under Fischer and

Schornberg’s analysis, profitability is obviously a significant variable for assessing

sector competitiveness and value added as a percentage of turnovers is a kind of

profit margin that entity usually relies. “Market shares are often defined as the

proportion of the total available market segment or sales that is produced or sold by

a company. They also rationed that market share is a necessary competitive

indicator at the firm level even when analyzing aggregates, market share may be of

trouble” (InternationalJournal.org). Simply speaking, it can be said that

5

“competitiveness is how effectively an organization meets the wants and needs of

customers relative to others that offer similar goods or services” (Operations

Management - MD021 www2.bc.edu). Normally, three competitive levels are

focused: country, industry, and firm level. Originated from a Latin word –

Competer – involvement in a business competition for markets, competitiveness is

now broadly used across different fields. This study is focused on firm-level

competitiveness. It can be defined as the ability of firms to design, produce or create

markets products/ services superior to those offered by rivals. Among the three

competitiveness levels, firm level is of greatest interest in practitioners and has

attracted the maximum attention of researchers. Michael Porter says “it is the firms,

not nations, which compete in international markets”. The firms actually compete in

the global stage and cope with the direct competition.

Some competitive dimensions that firms should focus as below:

Cost

Product Quality and Reliability

Delivery Speed

Delivery Reliability

Sales and after sales service

Coping with Changes in Demand

Flexibility and New Product Introduction Speed

Other Product-Specific Criteria

1.2 Sources of competitiveness

The identification of sources of competitiveness has been supported by known

perspectives on competitiveness. According to Dr Ajitabh Ambastha and Dr. K.

Momaya, select connotations of firm level competitiveness from literature review

provide richer and comprehensive views on sources of competitiveness.

Table 1.1: Selected connotations of firm level competitiveness:

No.

Source

6

1

Brand and reputation

2

Culture and system

3

Human resources

4

Technology & IT applications

5

Value creation

6

Customer satisfaction

7

Market share

8

Productivity and new product development

9

Price, expenses

10

Marketing

11

Relationships

12

Others…

Competitiveness can be viewed via competency and environment approach. The

role of external factors (economic, legal, technological… factors) and internal

factors (firm’s strategy, structures, human resources, competencies, and other

tangible and intangible resources for their competitive success) should be

emphasized.

In today’s turbulent business environment, dynamic capabilities, flexibility, speed

and adaptability are becoming more significant sources of competitiveness. These

kinds of sources will be clarified more through analysis models in the part 1.3

below.

1.3 Models to assess and analyze industrial competitive environment

In essence, the duty of leading manager is to understand and cope with competition,

or in other words, work with competitiveness. However, they often define so-called

rivalry too narrowly, as if it happened only among direct competitors. Yet the

matter of competitiveness goes beyond direct competitors certainly. In order to

7

estimate competitiveness, it is essential to have analyses in both external and

internal environment.

The external environment has two aspects: macro and micro environment. Macro

environment deals with things affecting all the firms in the economy, whereas micro

environment deals with things that affect firms in specific industries. PEST model

(Economic, Political, Technological, Social factors…) is widely used to analyze

macro environment; and Michael Porter’s five competitive forces model (Rivalry,

Potential competitors, Customers, Suppliers, and Substitute) is mostly used to

analyze industry environment.

1.3.1 PEST analysis

PEST stands for Political, Economic, Social and Technological factors. However,

the number of PEST analysis is unlimited. Other country-specific factors can be

added to perform macro environment.

Economic factor:

Economic growth/ growth rate

Inflation

Monetary policy and exchange rate

Government intervention

Government spending

National income

Unemployment rate, and others

Political factor:

Legal framework

Regulations and tariffs

Taxation

Political stability

Intellectual property and consumer protection, and others

Technological factor:

Technology transfer

8

Impact of changes in Information Technology on economy and

industry

New discoveries and development

Capabilities of application and customization, and others

Social –cultural factor:

Culture

People attitude (to work, health, safety…)

Living conditions

Lifestyle

Education, and others

Other factors:

Natural factor (territorial area, level of rain, typhoons, storms,

climate…)

Demographical factor (ages, numbers of young, birth rate, death

rate…)

1.3.2 Five Force analysis

Michael Porter’s five competitive forces include industry rivals, buyers, suppliers,

potential entrants and substitute products. The five competitive forces shall help

define an industry’s structure as form the nature of competitive interaction within an

industry.

9

Table 1.2: The five forces that shape industry competition of Michael Porter.

Rivalry among existing competitors

When the rivalry is high, the profitability of an industry is limited. The industry

profit which driven down by rivalry depends firstly on intensity with which firms

compete and secondly on the basis on which they do.

Firstly, the strength of rivalry reflects the intensity of rivalry, which is due to:

The number of competitors

The growth rate of industry

High exit barriers

Competitors’ high commitment to the business

Firm lacks of familiarity with one another (diverse approaches or

differing goals)

10

However, the strength of rivalry also reflects the basis, or the dimensions on which

rivalry occurs. Once competitors compete on the same basis, it will have a major

influence on profitability.

In rivalry, price war is the destructive factor to profitability as price competition as

it helps transfer profits from an industry to its own customers. Price reduction also

interrupts buyers from product feature and service.

Price war happens if:

Products/services are identical and for customers there are few switching

costs; thus rivals can have price cut to attract more clients.

High fixed costs and low marginal costs, then players can cut price below

their average costs

There are still many rooms for capacity expansion. This capacity

expansion disturbs industry supply – demand balance, then often leads to

overcapacity and price reduction.

The product/service goes decline. This urges producers to cut price in

order to sell out product.

Not like price war, competition on other dimensions such as product feature,

customer service, delivery convenience, brand image, or promotions harm less to

profitability than price. Parallel, players can also improve value creation compared

to substitutes, or higher barriers to entry.

Another tragedy is whether rivals compete on the same dimensions. When most of

the players target to meet the same needs compete on the same dimensions

(attributes or basis), zero-sum competition is often visible, where one’s gain is

others’ loss; and then profitability is driven down.

Competition can increase average profitability or be positive when each player aims

to serve different customer segments, with different mixes of price, products,

services, features, or brand identities. Such positive rivalry can not only support

higher average profitability but also cause industry expansion, as the needs of more

and more buyers are met. With clearer understanding on competition, leaders

11

sometimes can take measures to go to a more positive direction of competition

nature.

Threat of new entrants

Newcomers to industry come with new capacity and efforts to achieve market share

which will set pressure on prices, costs and other factors. When new entrants are

entering into new markets, they can leverage current capabilities and cash flows to

warm up rivalry. Thus, the threat of entry puts pressure on the profit potential of an

industry. High threat of new entrants shall make current players cut down their

prices or boost investment to compete with new rivals.

The threat of new entrants in an industry depends on entry barriers and current

players’ reaction to newcomers. When low entry barriers go with little retaliation

from incumbents, the threat of entry goes high, therefore it holds down profitability.

There are 7 main sources of barriers to entry:

Supply-side economies of scale: Firm that manufactures or creates at

larger volumes will get lower costs per unit. Economies of scale in supply

affect entry by pushing newcomers to enter the industry on a large scale.

With the practice of value chain, economies of scale virtually in every

activity.

Network benefits of scale: When the customer willingness to pay for a

product/service rises with the number of other customers also patronizing

the company, network effects will arise in industry. Customers may put

their concern in larger firms for a product/service. Then network effects

constrain entry by limiting the customer willingness to buy from a new

entrant and by decreasing the price.

Buyer switching costs: The higher switching costs, the more difficult it

will be for newcomers to enter the industry.

Fund requirements: Large financial resources requirements also limit

entrance to the industry. The barrier is especially high if fund is required

12

for uncovered expenses. Huge funding requirements will constrain

newcomers, and vice versa.

Incumbency advantages independent of size: existing players always

have advantages to potential entrants (such as technology, geographic

locations, brand identities, experience…). And entrants have to try to

surpass such advantages.

Unequal access to distribution channels: Certainly, newcomers have to

seek for placement channels. The more placement channels the

incumbents keep, the harder entrance to an industry will happen.

Especially when barrier to distribution access is high, newcomers have to

cooperate to bypass distribution channels or create their own ones.

Restrictive government policy: Government can directly influence on

potential entry through tools such as restrictions, requirements,

regulations, taxation, subsidies…

Besides barrier to entry, expected retaliation also impact on the entry or exit to an

industry. Potential entrants will be limited by expected retaliation if:

Existing players have replied tough to newcomers previously.

Incumbents have resources that can limit entry (such as borrowing power,

redundant productive capacity, available distribution channels…)

Current firms can and intend to do price reduction to fill excess capacity.

Slow industry growth makes new entrants obtain market only by taking it

from the existing participants.

The power of suppliers

Power of suppliers is high when they can charge high prices, limit service or

quality, or shift costs to industry participants. Suppliers are powerful when:

The supplier group is more concentrated that the industry itself.

In terms of revenues or profits, suppliers do not depend much on the

industry (for example, suppliers provide inputs for several industries).

13

Industry players cope with switching costs when they want to change

suppliers.

The product/service offered by suppliers is differentiated.

No or few substitutes for what the supplier group is serving.

Threat when suppliers tend to enter the industry to become the industry’s

participants.

The power of customers

The power of buyers is high by forcing down prices, having negotiating leverage,

being price sensitive, or demanding better service and quality…

Customers have negotiating leverage when:

There are few clients or each one buy a large volume of product/service.

Product/service of the industry is standardized or undifferentiated.

Low switching costs in changing sellers for customers

Threat of buyers’ integration

A group of clients is price sensitive when:

There is a significant fraction of cost structure in the product. Hence,

customers can shop and bargain.

Cash-poor buyers

There is little affect by the industry’s product in the quality of customer’s

product/service.

There is little affect by the industry’s product in the client’s other costs.

With the high power of customers in non-life insurance industry, in one side, PJICO

and other companies have to face up with the threats of reduce price, benefit and in

other side, they have to supply much better service for customers.

The threat of substitutes

A product/service and its substitute perform the same function by a different means.

High threat of substitutes will suffer industry profitability. Substitutes place a

ceiling on prices. This threat is considered high when:

Substitutes have attractive price.

14

Low clients’ switching cost to the substitute.

Sometimes, industry changes can make substitutes attractive. And leading

management should pay enough attention in these changes.

1.4. Models to analyze firm competitiveness

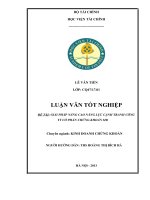

1.4.1 Value chain analysis

According to Michael Porter, value chain indicates the whole production chain from

the input to the output of final product/service by the end-user. There are two kinds

of activities in the value chain. One kind is called supporting activities, which

concerns the stream of production, where firms use its inputs, integrate and process

them, then produce or create its outputs. The other kind is called primary activities,

which are activities going across firms, where the outputs of one step become the

inputs of the next step.

Visible objectives of value chain can be mentioned:

Optimizing the overall activities of companies

Managing and coordinating the entire chain from initiate inputs to final

products/ services to end customers

Developing a sustainable competitive chain

Establishing choices and processes to support the relationships between

suppliers and customers…

Figure 1.1: Value chain

Source: www.manage12.com

15

Supporting activities include: firm infrastructure (finance, accounting…), human

resource management, technology development, and procurement.

Primary activities include: inbound logistics, production and/or operations,

outbound logistics, marketing and sales, and service.

A crucial analysis on the value created will help companies to identify its internal

capacity or its core competencies, and then figure out the strengths and weaknesses

of PJICO.

1.4.2 Core competencies assess

After extracting the strengths and weaknesses of firm from value chain analysis,

table of identification of sustainable competitive advantages to examine the long-

term or short-term strengths and weaknesses, and then they would lead to the

determination of core competencies for the company. The table is as follow:

Strengths/

Weaknesses

Valuable

Rare

Costly to

imitate

Big gap?

Coincide

with KSF

Marks

1. Factor 1

4/5

2. Factor 2

4/5

3. Factor 3

4/5

*KSF: Key Success Factors

Strengths with marks from 3/5 to 5/5 are considered as long-term strengths; whereas

short-term strengths are those with marks from 0/5 to 2/5. In contrast, weaknesses

with marks from 3/5 to 5/5 are short-term weaknesses; whereas long-term

weaknesses are those with marks from 0/5 to 2/5.

For the core competencies extracting from the sustainable competitive advantages

model, some possible solutions would be given based on improving strengths and

enhancing weaknesses, in order to improving competitiveness of the company.

16

CHAPTER 2: RESEARCH AND ANALYSIS

APPLICATION OF MODELS TO ANALYZE PJICO’s

COMPETITIVENESS

2.1 Overview of non-life insurance industry in general and in Vietnam

2.1.1. Non-life insurance industry in recent years

Non-life growth is still weak in industrialized countries, but strong in

Asia

In non-life insurance sector, premiums rose by 2.1% in 2010. Soft pricing still

showed slow growth in Europe and the US, while the strong economic rebound

pushed up premium growth in emerging Asia and the newly industrialized countries

in Asia. Throughout 2011, economic recovery is hopefully taking place, supporting

premium growth in both industrialized and emerging markets.

However, higher inflation, especially in the emerging markets, was chiefly driven

by rising food and energy prices. Emerging markets countries, especially in Asia,

weathered global financial recession better than most, due to sustainable growth in

GDP.

17

Table 2.1: Real growth rate of Industrialized and Emerging markets (1980 – 2009)

For non-life insurance in the world: global premiums growing, but only

slowly in the US and Western Europe

After global financial recession, the world premiums grew by 2.1% to USD 1819bn

in 2010. The recovery of capital in the non-life industry is still strengthening but

challenges also remain.

Developing countries: significant growth in many different markets

18

Table2.2: Real growth rate of insurance market of developing countries (1980 - 2010)

For South and East Asia: resilient despite the global financial crisis

Non-life premiums went up by 14% to USD75bn in 2009 (it was +9.7% in 2008).

Aggressive government fiscal policies and support has helped create pipeline of

projects on infrastructure construction, therefore, it helps non-life sector. Natural

disasters were not expected to be a main factor; however a number of typhoons hit

South and East Asia in the mid-years, causing lots of damages (Ketsana and

Miranae in 2009, Sansane in 2010…). The recovery from economic recession and

improving investment results also support non-life insurance. The major challenges,

like previous years, are continual price pressure, increasing inflation, and tighter

solvency standards.

19

Table 2.3: Asia Pacific Non-life markets at a glance, 2008 - 2010

Source: Swiss Re

Key concerns and conclusions of world’s non-life insurance:

The increase in interest rate, assets management is still existing problem

of insurance industry

The recovery of insurance companies’ financial states after recession

period

There are some breakthroughs in insurance industry: risk management

focus, bancassurance

Too many regulations that authority can apply for insurers, which can

distort development

Different development stages and different market segments among

countries, especially Asia